The Carrier Interest Tax Income Reform Debate

With no clear or definitive indication of how the “carried interest income tax loophole” issue may be changed or addressed in tax reform from the Ways and Means House blueprint, we can discuss it based on the last proposal that was put forward in 2010. This proposal was the last piece of legislation that seriously debated carried interest tax rate. Based on the 2010 plan, many business owners, limited liability (LLC) companies and active participants in partnerships could possibly face dramatically higher income tax burdens that would require certain income to be taxed at ordinary rates, subject to self-employment taxes. Now historically, this type of income has been characterized and as capital gains. The 2010 legislation is directed at investment services partnership interests (ISPIs), also known as “carrier interest” or “profit interest” and is aimed at individuals who make their living in real estate, venture capital, and or private equity businesses. Many real estate partnerships allow for the developer to receive a portion of profits from the property once agreed-upon returns to the investors are met.

With no clear or definitive indication of how the “carried interest income tax loophole” issue may be changed or addressed in tax reform from the Ways and Means House blueprint, we can discuss it based on the last proposal that was put forward in 2010. This proposal was the last piece of legislation that seriously debated carried interest tax rate. Based on the 2010 plan, many business owners, limited liability (LLC) companies and active participants in partnerships could possibly face dramatically higher income tax burdens that would require certain income to be taxed at ordinary rates, subject to self-employment taxes. Now historically, this type of income has been characterized and as capital gains. The 2010 legislation is directed at investment services partnership interests (ISPIs), also known as “carrier interest” or “profit interest” and is aimed at individuals who make their living in real estate, venture capital, and or private equity businesses. Many real estate partnerships allow for the developer to receive a portion of profits from the property once agreed-upon returns to the investors are met.

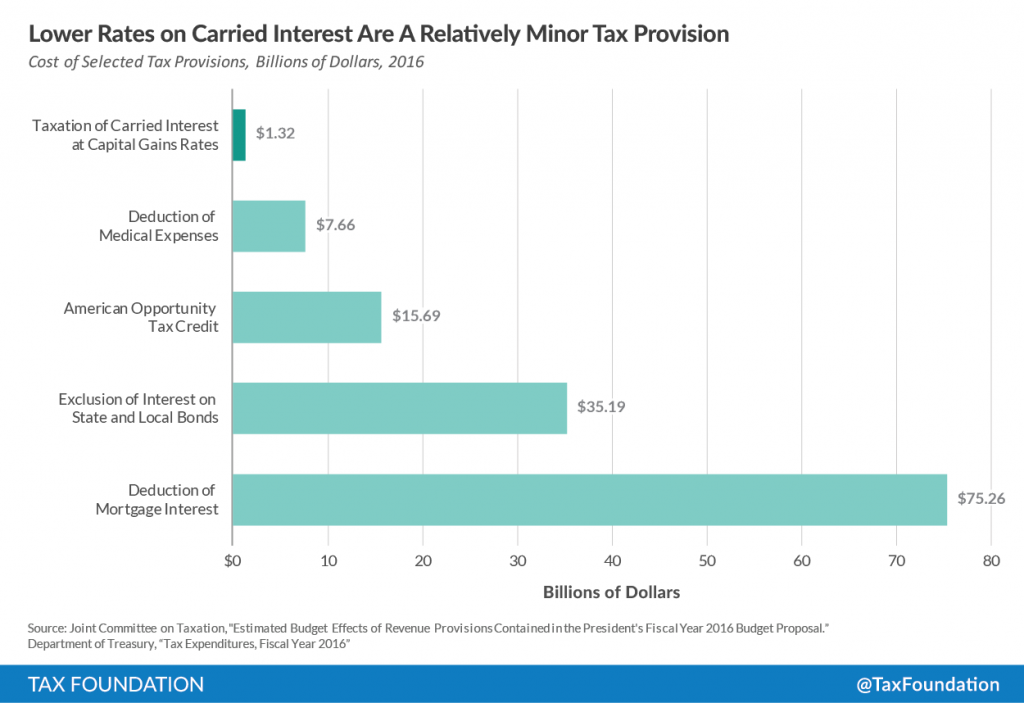

Why is this controversial: The “carried-interest” tax loophole allows managers of certain private-equity funds to treat the bulk of their earnings as long-term capital gains. The current tax rate on capital gains for higher-income earners is 20 percent; the ordinary tax rate for the same class is 39.6 percent.

Under the 2010 proposal, partnership income allocable to ISPIs subject to the new law in the year of enactment will be lesser of either: (1) income for the year or (2) income after the date of enactment. Furthermore, if an interest in an ISPI is sold after the date of enactment, the loss or gain on disposition would be subject to the new law. In addition, there is no distinction for partnership interest acquired before or after the date of enactment. Consequently, a transaction resulting in long-term capital gain being recognized in 2017 before enactment would be subject to a federal rate of 20%. So if it is recognized after enactment- either through allocable income or the sale of the interest in the ISPI- it could be subject to taxation at ordinary rates, possibly ranging anywhere from 33 to 39.6 % (39.6 % is currently the maximum federal rate). As a result, if passage of similar carried interest tax reform legislation under the Trump Administration appears, imminent, partners may want to recognize any built-in long-term capital gains prior to enactment of this law.

Under the 2010 proposal, partnership income allocable to ISPIs subject to the new law in the year of enactment will be lesser of either: (1) income for the year or (2) income after the date of enactment. Furthermore, if an interest in an ISPI is sold after the date of enactment, the loss or gain on disposition would be subject to the new law. In addition, there is no distinction for partnership interest acquired before or after the date of enactment. Consequently, a transaction resulting in long-term capital gain being recognized in 2017 before enactment would be subject to a federal rate of 20%. So if it is recognized after enactment- either through allocable income or the sale of the interest in the ISPI- it could be subject to taxation at ordinary rates, possibly ranging anywhere from 33 to 39.6 % (39.6 % is currently the maximum federal rate). As a result, if passage of similar carried interest tax reform legislation under the Trump Administration appears, imminent, partners may want to recognize any built-in long-term capital gains prior to enactment of this law.

Investment Services Partnership and Qualified Capital Interest

The 2010 proposal would create Section 710 of the internal Revenue Code. Section 710 would define an ISPI as any interest in a partnership held directly or indirectly by any person, if it was reasonably expected at the time the interest was acquired that such person (or any related person) would provide, Directly or indirectly, a substantial quantity of any of the following services with respect to the assets held (directly or indirectly) by the partnership. By the partnership:

- Advising on, investing in, purchasing, or selling any specified asset;

- Managing, acquiring, or disposing of any specified asset;

- Arranging financing with respect to acquiring specified assets; or

- Any activity in support of any service described above.

Although, partner holding an ISPI could escape the higher tax rate on a qualified capital interest (QCI). Usually, a QCI would be acquired upon the contribution of allocations of partnership items in a similar manner as those made to partners not holding an ISPI. If a new bill passes written with the same legislative terms as in 2010, guidance will be clarify certain matters, including when all partnership items are allocated to partners in the same manner and all partners provide services.

Here is an Example

Say there is a partnership that has a capital asset that could be sold for $20 million encumbered with debt of $18 million. The partnership’s income tax basis in the asset is $10 million. Interest considered ISPIs own 20 percent and QCIs own 80 percent. Below are the results to the holders of the ISPIs if the asset is sold before or after enactment of the new bill

| Before enactment | After enactment | |

| Proceeds to ISPI partners | $ 400,000 | $ 400,000 |

| Federal income taxes ** | $ (400,000) | $ (660,000) |

| Net after tax proceeds/(cost) | $— | $ (260,000) |

** Assumes a 20 percent capital gain rate and a 33 percent ordinary rate following tax reform

Here is a Planning Consideration

Most likely any carrier interest provision would apply to sales and dispositions of ISPIs after the date of enactment. There may be a chance to lock in appreciation in an ISPI at capital gains rates if a transaction can be executed before tax reform becomes effective. Given that the tax reform process is in the early stages, and what provisions will ultimately be included is not known yet, we don’t suggest any restructuring at this moment. We do recommend that you identify such interest for possible planning, and look to see what restrictions and approvals you may need to transfer such interest so that you have sufficient time to execute transfers if such tax provisions advance.

Conclusion

Any of these suggested tax reform plans will have to be negotiated in Congress. The House Ways and Means Committee has its Tax Blueprint, which, while similar, does differ from the president-elect’s proposals. It is unclear how Senate proposals could affect reform. In the meantime, taxpayers should be prepared and ready to adapt to forthcoming changes

To learn more information on this corporate tax topic, or to learn how Thomas Huckabee, CPA can help. Contact us for a free consultation

{kind=link}