Should investments in intangible assets be counted more on a company’s balance sheet in a post Covid-19 digitized world?

Recently PWC published a report titled “The unbalanced balance sheet: Making intangibles count” that points out that in many industries business models have been continuously evolving over the past decade that are delivering economic value from making investments in intangible assets, such as brand value, technology and customer relationships. And they are making the argument that this intangible-centric approach has been accelerated and become more apparent since the Covid-19 pandemic has pushed the digitization of the economy forward.

- research and invest in new technologies,

- cultivate customer relationships that form the basis for future revenue streams,

- foster relationships with partners and service providers that complement in-house capabilities,

- run advertising and promotions that enhance product recognition and brand affinity,

- Identify, hire, and nurture a workforce that can efficiently and effectively deliver on the company’s value proposition, or

- develop strong processes, know-how, and trade-secrets that create efficiencies and value.

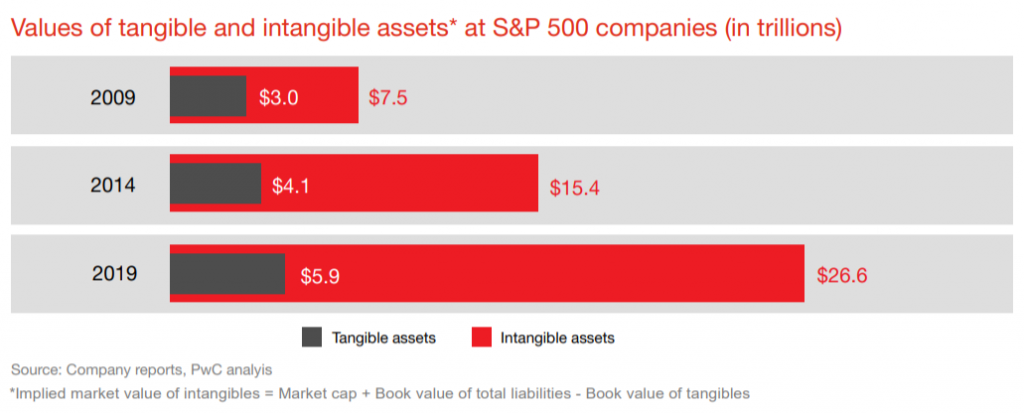

According to their research “since 2009, the implied market value of intangible assets at S&P 500 companies increased 255%, while the book value of tangible assets only increased 97% over the same period.”

(image credit: PWC)

In September of 2020, Jason Thomas the Head of Global Research of the Carlyle Group, Global Insights division published a white paper report titled “When the Future Arrives Early”. In this report Mr. Thomas discusses how technology-enabled adaptation has opened the door to more sweeping changes in business models and strategies. In this report there are few important takeaways for business owners and investors to understand.

- The most consequential innovation of the past twenty years may not be a specific application or device, but instead the way that technology facilitated the emergence of new business models. The technology sector’s outperformance over the past decade largely reflects the fact that many of the software, internet and data analytics firms have asset-light business models with market values that depend largely, if not entirely, on intangible assets. In hindsight, 2020 may be the year that “technology” stopped being thought of as a sector in its own right and more of the key differentiator between all companies irrespective of industry.

- The emergence and growth of ‘virtual’ businesses provided conspicuous evidence that, in the digital age, value accrues to ideas, R&D, brands, content, data and human capital— i.e. intangible assets— rather than industrial machinery, factories or other physical assets.

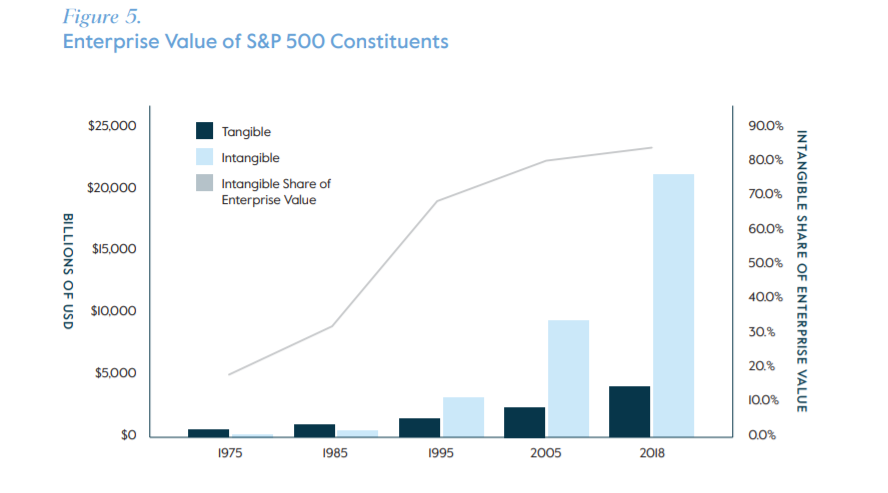

- In the digital age, this paradigm no longer holds. Current accounting rules do not allow internally generated intangible assets to be capitalized and recorded on balance sheets. As a result, intangible assets account for nearly 85% of corporate enterprise value (Figure 5, above), but are not reflected in the book value unless they are acquired and characterized as goodwill.15 These missing assets have not only caused price-to-book to lose its explanatory power, but caused the historical relationship to reverse over the past decade.

(image credit: Barclays Global)

While this value creation has happened, the accounting model has remained unchanged. Current accounting guidance does not always recognize the value created by intangibles, either on the balance sheet or in the footnotes. Although hard assets, such as property and equipment, appear on company balance sheets, investments in internally-generated intangibles are generally expensed as incurred. As a result, a company’s most valuable assets often do not appear on its balance sheet. The result can be a large gap between the book value of the company and its market capitalization. In 2019 I wrote an article titled “Do financial statements really work for digital technology startup corporations?” which is closely related to this article and still begs the question. Does financial reporting need to be enhanced to reflect the transition to a knowledge-based economy and highlight greater insights into a company’s intangible investments?

The PWC report states that the “communicating this information as part of the financial reporting process, rather than through other avenues, subjects it to the rigorous processes and controls in the financial reporting ecosystem that are designed to produce information that is reliable, consistent from year to year, and comparable between companies.” and it goes further to point out the importance of this concept as investors are increasingly focused on a company’s environmental, social, and governance (ESG) strategy, which highlights management’s stewardship of certain intangibles, such as human capital. But even as sustainability and investing companies that are doing this has become en vogue investing buzzword, CNBC recently reported a that Tariq Fancy, former BlackRock CIO of sustainable investing, wrote an op-ed in USA Today stating that “the financial services industry is duping the American public with pro-environment, sustainable investing practices.” He says there is no evidence ESG investing has any social impact. I guess it will be up for debate about how governments and companies tackle climate change but this another topic altogether.

How can financial statements most effectively and efficiently communicate information about intangible assets to stakeholders?

Given the vast scope of different kinds of intangibles, there may not be a one-size-fits-all approach. The PWC report stated that Instead, stakeholders may need to work together to develop a mixed model of recognition and disclosure to communicate the relevant decision-analysis information.

So what is the value of intangibles?

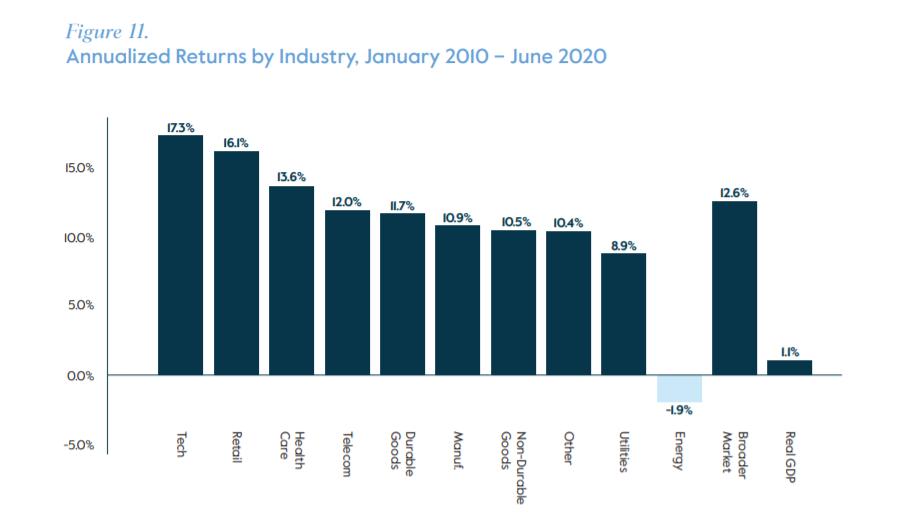

The increasing proportion of company value represented by intangible assets reflects not only greater investment, but also some attributes of these assets that may make a company worth more than its book value. Just look at how many digital technology enabled and cloud based business model companies have outperformed others that have not made similar investments. In the Carlyle Group white paper, . They mention, that the technology sector’s outperformance over the past decade (Figure 11) largely reflects the fact that so many of the software, internet and data analytics firms in the space have “asset light” business models with market values that depend largely, if not entirely, on intangibles like human capital, R&D, and proprietary data and technology.

(image credit: Barclays Global)

Many intangible assets, such as certain technologies, are infinitely-scalable, meaning they can be deployed in additional situations for no or little additional cost; as a result, their economies of scale often dwarf those that can be achieved through tangible assets. In addition, some intangibles, such as patents, are unique and protected by legal or other barriers to competition, thereby enhancing their value. Despite the extraordinary value of intangibles, financial statements are generally not designed to directly capture and communicate information related to them unless they arise in connection with the acquisition of a business. In fact, the financial reporting ecosystem as a whole devotes minimal attention to assets that are not recognized on the balance sheet, such as internally-generated intangibles.

What are the inconsistencies in accounting models for investments?

(image credit: PWC)

Today’s financial reporting model evolved over time, resulting in inconsistent accounting for different types of investments even though management applies a similar capital allocation process to all significant investments. The result: GAAP earnings metrics reflect the return on other investments, but not internally-generated intangible assets. As a result of the non-recognition of internally-generated intangibles, the company value created by investing in intangible assets is only observable to stakeholders in an indirect, lagging way (for example, through growing revenues or expanding margins). Similarly, there is only indirect information about management’s stewardship of those assets. Decoupling an expenditure from the associated economic benefit—as we do for internally-generated intangibles—may drive users to other data sources to assess value creation and preservation, calling into question the relevance of the financial statements.

The End of Accounting and the Path Forward for Investors and Managers

Investors are already beginning to get their information elsewhere. In 2016, Baruch Lev and Feng Gu wrote a book called “The End of Accounting and the Path Forward for Investors and Managers” and argued that Investors are poorly served by arcane accounting methods, and that new ways are needed to measure companies’ performance. In an excerpt from the book in the WSJ, the authors explain

“Most analysts’ and institutional investors’ questions in conference calls with corporate managers and in “investors’ days” are about the metrics missing from financial reports precisely because accounting standards do not require them. It is metrics like customer growth and churn rate, test results of products under development, policy renewal and cancellation rates of insurers, or capacity utilization of transportation companies, that reflect the business strategy and its execution, rather than reported assets, liabilities or profits.”

The problem they argue is that ‘rank-and-file investors’ still take reported earnings seriously, as clearly indicated by share-price declines upon announcements of earnings missing consensus analyst estimates (declines that are often quickly reversed, locking in investors’ losses). Rather than leveling the playing field, deficient financial reports exacerbate information differences and disparities in investment gains among investors.

In other words, only few deep-pocketed investors have direct access to corporate managers and can afford research teams using expensive real-time data (weekly drug prescription sales, or satellite scanning of retailers’ parking lots), while most investors still rely on deficient accounting reports.

So what is the path forward

As financial reporting continues to mature, the accounting hallmark of relevance must be a key component of the financial reporting framework. We believe information about intangibles is becoming increasingly important to maintaining the relevance of financial reporting in the new economy, where intangibles represent such a large portion of many companies’ value and often reflect some of their most significant investment decisions.

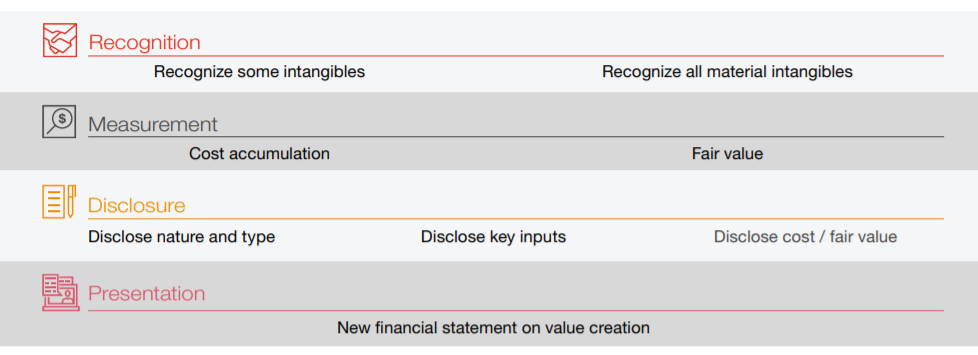

Given the complexity and evolving nature of intangibles and diversity in how companies manage intangibles and investors evaluate them, there may not be a one-size-fits-all approach. There is a wide range of alternatives to providing decision-useful information to investors, which could include recognition of all or some material intangibles, whether at cost or fair value, disclosure of key intangibles in addition to or instead of recognition, or even a new financial statement that provides measure of value creation. Each of these alternatives has different information needs and benefits, and some information is already captured. Companies already track the cost and return information, such as intellectual property (IP), using a cost accumulation approach. Also, they closely track IP for legal, tax, and other purposes such as ESG reporting, and often explicitly consider their return on investment when deciding which IP projects to fund.

In addition, companies in some industries already supply information on key drivers of the value of assets such as customer relationships. For example, companies with a subscription-based business model will often disclose customer attrition data. Another source of disclosure information for certain intangibles, such as workforce assets, is information increasingly contemplated in ESG disclosures.

(image credit: PWC)

Conclusion

Samuel J. Palmisano, Former Chairman, CEO, and President, IBM once said “utilizing and valuing intangible assets is essential for companies’ investment and capital allocation decisions. Finding an approach that could allow managers and investors to appraise intangibles and thereby more accurately assess a company’s value and performance would be useful.” Transformational changes to the financial statements, such as recording and/or disclosing all or some internally-generated intangible assets, pursued with a high degree of business community engagement, will help the financial reporting process keep pace with business innovation and remain relevant. Maintaining relevance is a continuous process. The nature of the information captured in the financial statements needs to continue to evolve, and the best approach to communicating information on value creation may change over time. We should not wait to begin the conversation on how to communicate this important information to stakeholders.

Thomas Huckabee CPA provides accounting services for technology companies in San Diego, and if you have any questions, feel free to contact us for a free consultation.

{kind=link}