Managing cash flow liquidity during uncertain recessionary time periods such as Coronavirus

According to a recent Harvard Business School Working Knowledge article, small-business owners that are trying to weather the Coronavirus pandemic will face a financial blow that’s likely to be worse than what they experienced during the Great Recession more than a decade ago, says Karen G. Mills, senior fellow at Harvard Business School. Mrs Mills who led the United States Small Business Administration from 2009 to 2013 say’s “this is going to be orders of magnitude worse than the financial crisis, many small businesses will not survive more than a month.”

In the wake of this Coronavirus shutdown, many corporations are dealing with disruptions to customer demand and supply chains, workforce and labor issues, and new risks to business processes and information systems. With many business leaders not used to managing during disruption, they may need assistance in prioritizing decision-making during times of crisis.

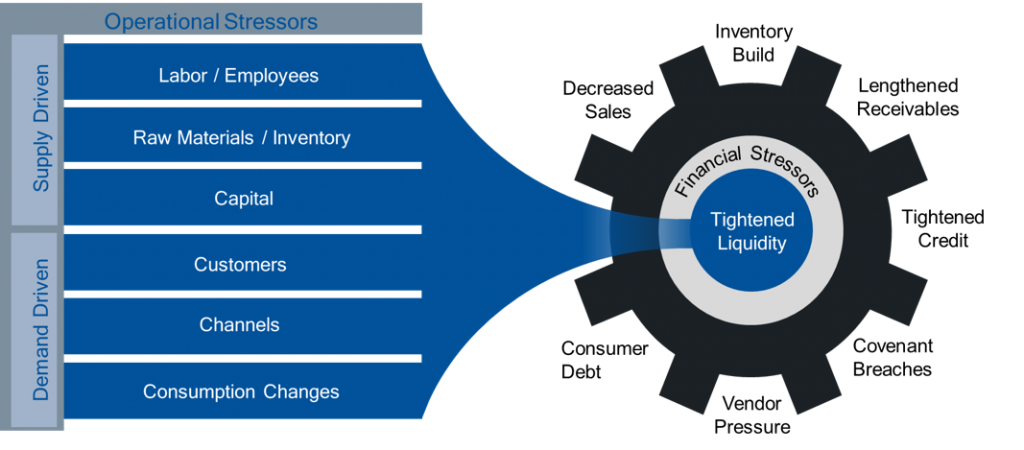

When the economy goes from a chugging along at a decent rate of GDP growth and consumer spending to one of a temporary shutdown and uncertainty in a relatively short time, the pressure on your organization is real and overwhelming. Two main issues that many businesses face is cash flow issues and supply chain disruptions from raw materials to finished products. What is cash flow? Cash flow is a snapshot of your business finances taken during a specific time period. It provides a picture of money flowing into and out of your business, letting you know how liquid and flexible your enterprise is, while gauging its relative long-term health.

When the economy goes from a chugging along at a decent rate of GDP growth and consumer spending to one of a temporary shutdown and uncertainty in a relatively short time, the pressure on your organization is real and overwhelming. Two main issues that many businesses face is cash flow issues and supply chain disruptions from raw materials to finished products. What is cash flow? Cash flow is a snapshot of your business finances taken during a specific time period. It provides a picture of money flowing into and out of your business, letting you know how liquid and flexible your enterprise is, while gauging its relative long-term health.

The Big 4 accounting firm Deloitte recently published an article about how to manage cash during this crisis. If you have ever read my blog before some of my favorite subjects are on working capital optimization, and cash flow management tips. Taking proactive measures to understand your company’s cash flow should be made a crucial task as you navigate the market over the next few months. Whether you apply for some of the Cares Act stimulus relief loans, it takes cash flowing in, rather than net bookings, to meet your businesses financial obligations and ride the wave of this potential downturn. In a post about cash flow from Baker Tilly, it mentions that in slowing periods like this, relying on normal finance and accounting metrics such as “net income, net operating cash flow, and earnings before interest, tax, depreciation and amortization (EBITDA) can be misleading and dangerous during times of declining sales and economic calamity.”

The JPMorgan Chase Institute estimates (pdf) that the average small business has 27 days of cash in reserve, but Main Street businesses often have less than 20 days’ worth. While forecasts vary, many public health experts don’t expect the coronavirus outbreak to subside for at least eight weeks, assuming that social distancing and other mitigation efforts can slow the spread.

Responding to the immediate challenge

The Deloitte article suggests organizations can look back at some of the lessons “learned from the 2003 SARS outbreak, the 2008 recession and credit crunch, and the last black swan event to significantly impact global supply chains–the Japanese earthquake of 2011.” They offer the following best practices and strategies for consideration:

- Make sure you have a robust framework for managing supply chain risk

- Make sure that your own financing remains viable

- Pay special attention on the cash-to-cash conversion cycle

- Think like a CFO, across the organization

- Revisit your variable costs

- Revisit capital investment plans

- Focus on inventory management

- Extend payables, in a strategic manner

- Manage and expedite receivables

- Consider alternative supply chain financing options

- Audit payables and receivables transactions

- Understand your business interruption insurance

- Consider alternative or non-traditional revenue streams

- Convert fixed to variable costs, where possible

- Think beyond your four walls

If your company utilizes any of these cash management strategies, then you may be able to increase your available cash towards the end of this Coronavirus shutdown. What are some of the strategies that businesses can use. Many companies are using abrupt cost cutting reductions and reducing their investments in net working capital (inventory) while also converting assets (accounts receivable) into cash.

The Baker Tilly article makes a comparison of this financial analysis is similar “to an airplane taking flight requiring both speed and altitude – you must optimize both the balance sheet and operations simultaneously. To accomplish this, a thorough understanding of your operating cash cycle along with your fixed and variable cash obligations is necessary.”

Start by developing a robust short term 12-week cash flow forecasting model

The firm Baker Tilly recommends that companies should run a 12-week cash flow analysis model to help figure out some of the crucial financial decisions your company will need to make during these unprecedented times. Performing a cash flow analysis can give you and your bank lenders a better view of your company’s next 90 days’, uses and cash positions.

For many types of businesses, examining a 3 month time period, can give good look around a company’s operating cash cycle and show financial details of all all cash inflows, outflows and its ability to meet financial obligations as they come due. This type of cash flow analysis will account for where cash is produced and spent and the resulting expected cash position over next few months. Doing this will help to spot any potential risk areas of cash shortfalls beforehand, so you can make changes accordingly. Cash flow analysis services help management teams have more confidence when making capital or operational decisions during times of deteriorating business activity. This is especially relevant during this temporary government shutdown of “non essential businesses”, where uncertainty surrounding liquidity and solvency is leading to a critical need for visibility of cash availability to meet needs such as debt service, material purchases and payroll.

Finance and liquidity

As business activities slow, some companies are seeing lower revenue resulting in less cash flow, managing the global cash and liquidity position will be crucial in the weeks ahead. In an article from PWC, titled “what US business leaders should know” they make a few suggestions:

- Model the worst-case scenarios to assess the impact on the cash position, and revise often

- Identify the financial and operational levers that can be pulled to conserve and generate cash, and potentially increase access to funding

- Understand and plan for the financial reporting considerations that will result from the Coronavirus

- Assess prospects for relief from the tax provisions or other measures in US economic stabilization package

Use the financial data to make smart decisions

Most industries are being affected and disrupted in this current environment besides, companies being named as essential (such as grocery stores, medical suppliers, home improvement stores, pharmacies, liquor stores and some online ecommerce and subscription businesses) so it never been more vital to have the most up-to-date and current information available to you. By monitoring and reporting on a weekly basis, you can obtain pertinent info in advance of the typical monthly financial close process in order to make nimble, informed decisions. Many small, medium and even large businesses are being forced make very difficult decisions such a retail companies like Macy’s having to furlough 130k workers, and close stores. Some of these decisions and activities can also include:

- customer credits and discounts

- fixed and variable cost reductions

- supplier terms negotiations

- lender negotiations

- landlord negotiations

- organizational changes

- federal and state stimulus program applications and other such items

Balancing cost cuts to avoid risks that could cause long-term losses

Every business is trying to survive and stay solvent during the next coming weeks by either accessing some the government relief stimulus, or by cutting costs to try to protect their revenue’s cash and profits, The problem is that although this might be an essential move, using the wrong approach could leave your company open to critical losses. Grant Thornton published a useful article titled “Manage the tension of revenue, risk and COVID-19“and the Bryan C. Moser suggests “Leaders must resist the temptation to cut risk management and compliance functions so deeply that longer-term business consequences are even more severe.” They suggest possibly conducting a general risk assessment, to get a more clear perspective, to find specific risks that could lead to claims or other disputes – such as supply chain issues that might block you from fulfilling contractual commitments and other parts of business operations.

Once your legal and financial analysis pinpoints your companies most exposed areas of risk, confirm that your team is diligent about their daily documentation and interactions:

- Maintain clearly documented financial records of costs incurred or losses resulting from specific incidents

- Understand costs associated with not meeting your commitments

- Document actions taken and costs incurred to mitigate circumstances

- Know your suppliers well enough to assess whether they will be able to deliver

- Examine supply chain and other vendor agreements to find opportunities to maintain cash

Make sure you still maintain strong compliance controls which will help set the tone for ethical and prudent cost cutting decisions or pivots (such as temporarily making PPE equipment for hospitals etc) across the enterprise.

Here are some proactive steps you can take

Grant Thornton suggests working with your legal and financial advisors, and then implement some proactive steps to mitigate the impacts of future regulatory enforcement and other potential developments:

- Assess the business functions under the greatest stress (such as logistical disruption or revenue pressure in the sales function)

- Identify the regulatory and compliance risks facing each identified business function

- Ensure proactive action on compliance controls, such as training and ongoing monitoring

- Deliver off-schedule risk-based compliance training and enhance risk-based on-monitoring efforts

- Consider risk-based off-schedule compliance reviews or audits

Conclusion

Cash flow management should to be an integrated component of a corporation’s overall Coronavirus risk assessment and action planning in the next few weeks. Though you should cautious when executing quick cost cuts that can expose significant risks. As executives and managers feel the pressure to swiftly scrutinize non-revenue-generating activities, it’s important to understand where cuts could have a devastating impact on legal or compliance functions – either directly or as a side-effect of pulling a long-established thread of compliance from the fabric of the company.

Even for organizations that have not yet been drastically affected by it, It is recommended that management teams with any concerns about Coronavirus economic impact should proactively evaluate their cash flow requirements, and develop appropriate actions under various potential scenarios, and assess potential risks in and to their customer base and supplier chain network. If you are a startup you need to focus on your capital, your balance sheet, liquidity and your customers ultimately.

We understand these circumstances are unique and unprecedented for you. Prioritizing your information as you navigate very difficult business decisions will provide a level of stability moving forward. If you are business in Southern California contact Huckabee CPA for free consultation about building out a cash flow analysis for your company.

{kind=link}