CARES Act Tax Provision Modifications to NOL Carryback & Suspends TCJA 500k active losses limitation of pass-through entities

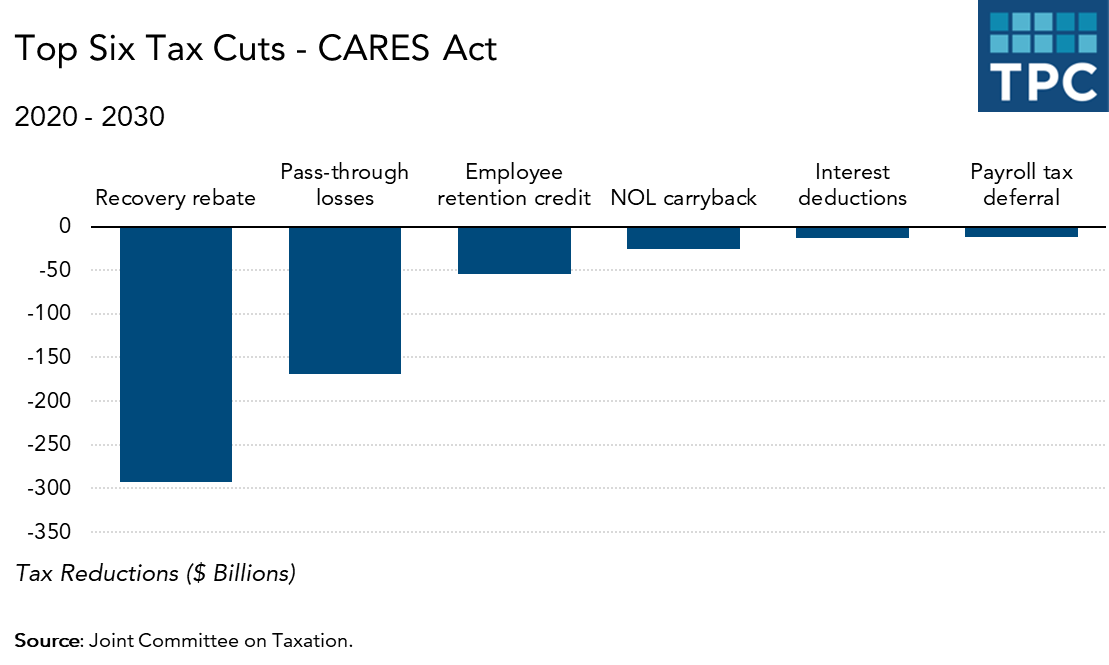

One of the recent questions that has come up in the news lately is who benefits from the CARES Act relief tax cuts? Its good question. And with the recent press about how a bunch of large publicly traded companies got millions in loans from the program meant for small business called Paycheck Protection Program (PPP). Recently a contributor Thorton Matheson published an article on Tax Policy Center, titled who benefits from the CARES Act tax cuts?, which found that the individual “recovery rebate” program will account for about half of the Coronavirus Aid, Relief and Economic Security (CARES) Act’s tax cuts. The TPC article found that nearly all of the remaining cuts will go to business, although workers may benefit from some of these. More than a quarter of the tax cuts go to taxpayers in the top income earners.

One of the recent questions that has come up in the news lately is who benefits from the CARES Act relief tax cuts? Its good question. And with the recent press about how a bunch of large publicly traded companies got millions in loans from the program meant for small business called Paycheck Protection Program (PPP). Recently a contributor Thorton Matheson published an article on Tax Policy Center, titled who benefits from the CARES Act tax cuts?, which found that the individual “recovery rebate” program will account for about half of the Coronavirus Aid, Relief and Economic Security (CARES) Act’s tax cuts. The TPC article found that nearly all of the remaining cuts will go to business, although workers may benefit from some of these. More than a quarter of the tax cuts go to taxpayers in the top income earners.

The recovery rebates will cost $292 billion, or 49 percent of the $591 billion 10-year cost of the CARES Act tax cuts. Which includes payments to individuals of $1,200 per adult ($2,400 per couple), plus $500 per dependent child under age 17, targeting the relief toward low and moderate-income households making $75,000 a year or ($150,000 per couple).

In Mr Matheson’s article he points out that “the next largest five tax cuts, totaling $276 billion or 47 percent of total CARES Act tax measures, are for businesses.” He goes on to add that “measures directly benefiting business owners—modifications of the tax treatment of net operating losses (NOLs), interest deductions, and active losses of pass-through entities—account for $209 billion or 35 percent. Two payroll-related measures—the employee retention credit and the employer payroll tax deferral—account for $67 billion, or 11 percent of total CARES Act tax cuts.” This relatively modest revenue cost reflects the expected repayment of the deferred payroll taxes in late 2021 and 2022.

Now many publications such as Forbes, CNN and the Washington Post have covered these Coronavirus stimulus tax law changes and they have said that these tax provision changes only benefit and apply to wealthy investors and business owners earning over $1,000,000 according to a report by the Joint Committee on Taxation (JCT), the nonpartisan congressional body. Regardless of your political point of view of these new tax breaks since it was a bipartisan bill that was passed. Lets get into how these new changes can help you as business owner or real estate investor save you more money or lower your tax liabilities.

SEC. 2304. Modification of Limitation on Losses for Taxpayers other than Corporations.

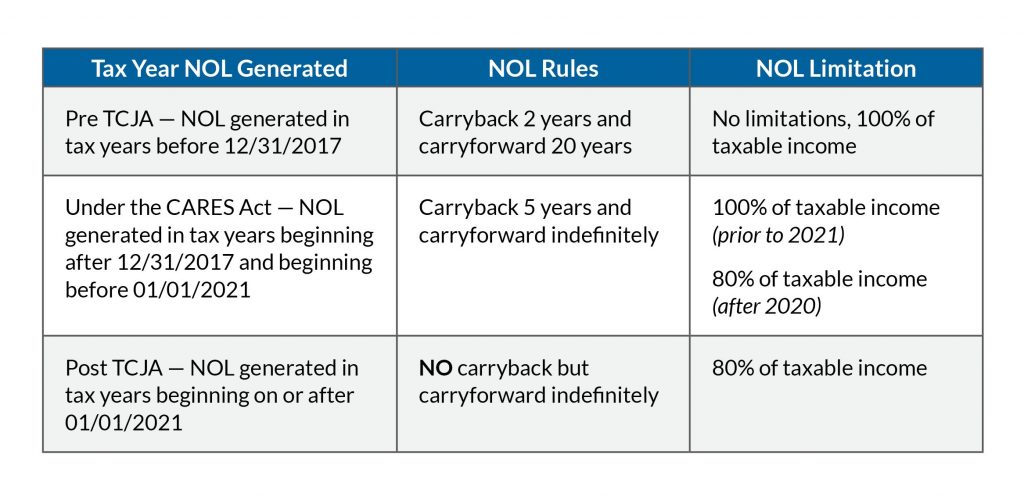

So previously when the 2017 Tax Cuts and Jobs Act tax reform (PL 115-97) was signed into law it changed the way non-corporate taxpayers can carry losses from a given year to minimize their tax bills in other years.

So beginning in tax year 2018, the TCJA law placed a limitation on taxpayers filing jointly so that they could only use $500,000 in depreciation deduction “losses” from actively-managed investments, like “pass-through entity” (such as S corporations and partnerships, as well as sole proprietors with “active” owners) income from businesses, to offset wage or capital gains income tax liability. As Senator Sheldon Whitehouse (D-RI), said in letter to Mike Pence and Steven Mnuchin:

“for example, if one spouse owns a company that had a $5 million loss in 2018 and the other spouse made $5 million from stock market investments, this limitation meant that the couple’s taxable income was $4.5 million (not zero, if the loss were allowed to fully cancel out the income). The other $4.5 million in losses, however, could be carried forward to use in future years.”

The CARES Act temporarily modifies the loss limitation for noncorporate taxpayers so they can deduct excess business losses arising in 2018, 2019, and 2020. (Code Sec. 461(l)(1), as amended by Act Sec. 2304(a))

So now under this change, a wealthy taxpayer couple (this applies only for individuals, not corporations) — can now deduct an unlimited amount of “excess losses” in real estate against income from other sources. So now real estate investors with high paying day jobs or large capital gains from other investments can potentially lower their tax bill significantly, like they could before the limits were put in place as part of the 2017 tax reform bill. The change applies to this year — and retroactively to 2019 and 2018. This means successful investors can file amended returns now, and get refunds of perhaps millions of dollars.

(image credit:Baker Tilly)

SEC. 2303. Modifications For Net Operating Losses

The Trump 2017 TCJA tax reform bill (PL 115-97) included another change that prohibits corporate and non-corporate taxpayers from carrying losses back in time. Before this change, a taxpayer that incurred a big loss in a given year could retroactively amend prior tax returns (going back up to five years) to use the losses to cancel out income, and thus to receive tax refunds. The 2017 TCJA law allowed losses to be carried forward indefinitely to future years but also slashed the amount of NOL income losses can offset to 80% of taxable income in a given year. Both of those changes hurt, especially the rule killing carrybacks. Sally b Schrieber ,a Journal of Accountancy contributor wrote an informative article on the recent NOL Carryback provision changes enacted by the Cares Act.

Thus, a taxpayer with $10 million in income would still have at least $2 million in taxable income, regardless of losses. But as a Forbes contributor Robert Woods states in an article titled IRS Allows Wide Use Of Net Operating Losses, Even Tax Refunds that part of the COVID-19 response, the new CARES Act helps in a big way. “for tax years starting after December 31, 2017 and before January 1, 2021—that’s 3 calendar years of losses that you incurred in 2018, 2019, or 2020—the new law reinstates and allows you to carryback 100% of these NOLs to the prior five tax years.”

- The CARES Act provides that NOLs arising in a tax year beginning after December 31, 2018 and before January 1, 2021 can be carried back to each of the five tax years preceding the tax year of such loss. (Code Sec. 172(b)(1) as amended by Act Sec. 2303(b)(1))

- The CARES Act temporarily removes the taxable income limitation to allow an NOL to fully offset income. (Code Sec. 172(a), as amended by Act Sec. 2303(a)(1))

Mr Woods states “losses that are carried back are carried to the earliest of the tax years to which the loss may be carried first. You have to work out the mechanics of claiming these, but it’s a sweet deal if you are in the sour position of having losses.” With COVID-19, there will be lots of business with losses for 2020.

Mr Woods states “losses that are carried back are carried to the earliest of the tax years to which the loss may be carried first. You have to work out the mechanics of claiming these, but it’s a sweet deal if you are in the sour position of having losses.” With COVID-19, there will be lots of business with losses for 2020.

For example, a corporate NOL from 2020 can be carried back to offset income from 2015, which may have been subject to a 35% tax rate rather than carried over to 2021 when income is subject to a 21% tax rate. In some cases, however, income in future years will be subject to higher tax rates than income in the carryback period, so you’ll need to work with your tax advisor to determine whether the carryback is right in your particular situation.

For example, a corporate NOL from 2020 can be carried back to offset income from 2015, which may have been subject to a 35% tax rate rather than carried over to 2021 when income is subject to a 21% tax rate. In some cases, however, income in future years will be subject to higher tax rates than income in the carryback period, so you’ll need to work with your tax advisor to determine whether the carryback is right in your particular situation.Mr Woods also brings up the question of what about Net Operating Loss carryforwards? He states that “CARES Act liberalizes the treatment those too, at least for time. If you want, you can waive the carryback, and can elect to carry NOLs forward to subsequent tax years.” He suggests that you have your CPA run the numbers to if it makes financial sense. In addition, for 2018, 2019 and 2020, corporate taxpayers can use NOLs to fully offset their taxable income, rather than only 80% of taxable income. For tax years beginning before 2021, taxpayers can take an NOL deduction equal to 100% of taxable income (rather than the present 80% limit).

What about after 2021?

For the tax years beginning after 2021, taxpayers will be eligible for:

- (1) a 100% deduction of NOLs arising in tax years before 2018, and

- (2) a deduction limited to 80% of taxable income for NOLs arising in tax years after 2017.

Under the changes of the CARES Act, corporate taxpayers with eligible NOLs may now be able to claim a refund for tax returns from prior tax years. For corporate taxpayers, NOLs carried back to pre-2018 years—when corporate tax rates were a whopping 35%—are more valuable than losses used to offset income taxable at the current 21% rate.

Thus, a corporation can carry back its 2018, 2019, and 2020 NOLs to offset pre-2018 ordinary income or capital gains that were taxed at rates of up to 35%. Mr Woods described it as “think of it as a kind of tax-rate arbitrage, so you can get a tax refund based on the old higher tax rate.”

IRS COVID Relief Guidance for taxpayers claiming NOLs

Recently another Forbes article mentioned that IRS provided guidance under the CARES Act to taxpayers with net operating losses. IR-2020-67, April 9, 2020 — “The Internal Revenue Service today issued guidance providing tax relief under the CARES Act for taxpayers with net operating losses. Recently the IRS issued tax relief for partnerships filing amended returns.”

For a more in-depth look at the guidance refer to PDF Revenue Procedure 2020-24. It refers to providing procedures for:

- waiving the carryback period in the case of a net operating loss arising in a taxable year beginning after Dec. 31, 2017, and before Jan. 1, 2021,

- disregarding certain amounts of foreign income subject to transition tax that would normally have been included as income during the five-year carryback period, and

- waiving a carryback period, reducing a carryback period, or revoking an election to waive a carryback period for a taxable year that began before Jan. 1, 2018, and ended after Dec. 31, 2017.

Six month extension of time for filing NOL forms

In Notice 2020-26 (PDF), the IRS grants a six-month extension of time to file Form 1045 or Form 1139, as applicable, with respect to the carryback of a net operating loss that arose in any taxable year that began during calendar year 2018 and that ended on or before June 30, 2019. Individuals, trusts, and estates would file Form 1045 (PDF), and corporations would file Form 1139 (PDF).

COVID relief for partnerships with NOLs

On April 8, 2020, the IRS issued Revenue Procedure 2020-23 (PDF), allowing eligible partnerships to file amended partnership returns using a Form 1065, U.S. Return of Partnership Income, by checking the “Amended Return” box and issuing amended Schedules K-1, Partner’s Share of Income, Deductions, Credits, to each of its partners. Partnerships filing these amended returns should write “FILED PURSUANT TO REV PROC 2020-23” at the top of the amended return.

Amended return considerations and estimating refunds

The CPA firm Grant Thorton provides an informative whitepaper about the Cares Act provision changes. And it they give a number suggestions to think about. The Cares Act contains numerous provisions that can immediately help entities stimulate cash flow. Entities should disclose in the period that includes March 27, 2020 the amount of refund they expect to generate if they plan to carry back NOLs to prior periods and if the entity can make a reasonable estimate of the refund amount. For example, the change in the IRC Section 163(j) limitation from 30 percent to 50 percent might create or increase an NOL that the entity will carry back to offset income in prior years.

However, at the balance-sheet date for the first quarter, the entity would probably not have finalized the 2019 computation of taxable income along with the amount of refund it expects to receive, but it should still disclose its best estimate of this refund amount if the amount can be reasonably estimated. In many cases, the provisions under the Cares Act may have multiple effects on an entity’s 2019 taxable income that should be assessed before the entity can determine the amount of the 2019 NOL it expects to generate. Further, the entity may still be determining whether to carry back or carry forward the NOL.

Conclusion

Please consult with a professional tax advisor regarding some of these considerations. However, given the potential offset to income taxed under a 35% federal rate, and the uncertainty regarding the long-term impact of the COVID-19 crisis on future earnings, it seems likely that most companies will take advantage of the revisions. And as a BDO summary article points out This is a technical point, but while the highest average federal rate was 35% before 2018, the highest marginal tax rate was 38.333% for taxable amounts between $15 million and $18.33 million. This was put in place as part of our progressive tax system to eliminate earlier benefits of the 34% tax rate. Companies may wish to revisit their tax accounting methodologies to defer income and accelerate deductions in order to maximize their current year losses to increase their NOL carrybacks to earlier years. Huckabee CPA here to help you take advantage of available tax savings to improve your cash flow situation and help your business take advantage of the inevitable opportunities that will arise as we emerge from the pandemic. Huckabee CPA can help determine if there are accounting method changes that can be filed to create additional losses that may be carried back to the applicable years.

There is a lot of information to absorb from COVID-19 implications and significant stimulus packages as companies focus on closing the first quarter of 2020. Congress has provided quite a few tax provisions that could help companies and investors generate cash flow during this uncertain time, If you are business owner in California, that has any questions or would like a free consultation fell free to contact Huckabee CPA.

{kind=link}