Here are 9 tax strategies investors may use to minimize taxes during a Democratically controlled administration

So as we found out in early January that the Democrats won the two special run off Senate seat races in Georgia, the powerful Senate governing body will be divided, 50-50. Which now gives them a narrow control of the Senate with the Vice President, Kamala Harris serving as a tie-breaker if the Senate is split on President Joe Biden’s Cabinet nominees or federal judges. The legislative filibuster effectively sets a 60-vote threshold to most controversial legislation, so Harris won’t be pressed into service there. An exception is a Senate rule that Republicans used in 2017, when the GOP controlled both chambers in Congress, to enact tax cuts. According to an Washington Examiner article Jim Manley, a former top aide to onetime Senate Majority Leader Harry Reid, a Nevada Democrat said that Harris’s most important vote “may be on the so-called reconciliation bills that will be used to pass some of [President-elect Joe Biden’s] tax and spending proposals.”

Recently William Baldwin, a senior Forbes contributor published an interesting article titled “12 tax angles for investors, what will survive the Democratic congress” he goes on to explain “tax-hungry legislators may go after incomes over $400,000. But they will likely leave in place a rich collection of avoidance devices. Here are ways that investors minimize damage from the IRS.” And as the President elect Joe Biden claimed on the campaign trail that are looking to undo parts of the parts of the 2017 Trump tax cut and, perhaps, to attack some of the long-standing tax lowering schemes that investors use. But Mr Baldwin, believes that most tax-wise investing strategies will probably survive because more than a few dodges have big fan bases among the voters. Those seem pretty safe. He mentions the notions of things that would fall under tax reform category such as taxing capital appreciation before an asset is sold. But he explains “implementing a mark-to-market scheme would be a nightmare of complexity, at least if any effort were made to keep very wealthy people from using loopholes that would be beyond the reach of the middle class.”

In the Forbes article, he explains that the easiest way to raise revenue is simply change the tax brackets, he cites Joseph D. Roberts, a senior wealth strategist at Rockefeller Capital Management thinks that Congress may explore these changes first. Such as:

- Increasing the top bracket from 37% to 39.6%

- increasing the corporate rate from 21% to 28%

- lowering the estate tax exemption to where it was before the 2017 tax cut

Mr Roberts says it’s unlikely that these hikes will be retroactive. So if this is the route the Democratic legislative tax writers go, there will be left in place numerous opportunities for savers to protect their capital. The Forbes article layouts 12 tax saving or planning techniques that wealthy business owners and investors should consider. I will cover 9 of them here.

1 Shuffle assets to avoid capital gains

(image credit: Charles Schwab)

(image credit: Charles Schwab)

Mr Baldwin mentions that here are a couple ways to sidestep capital gain taxes via an intra-family transfer. One is to give appreciated shares to a low-bracket relative who then sells. The other is to give the stock to an elderly relative who bequeaths it back to the donor, thereby capturing the step-up at death. To use either of these strategies you must know how to avoid certain pitfalls. You can move appreciated assets from this person to that person, in order to reduce or eliminate the tax on the capital gain.

One example he points out is a parent could transfer a winning stock position to their child to help them pay off college loans or buy a house. And they pick up the cost basis. If the child’s filing a joint return in 2021 and their taxable income (including the gain you’re handing off) is less than $80,800, then they’re capital gain tax rate is zero. He also mentions that with taxes, tricky rules surround this type of tax strategy. The stock has to be held for more than a year to get the benefit of the favorable rates on capital gains.

The kiddie tax is another rule to be aware of, which throws investment income back onto a parent’s tax return. There are various conditions under which the kiddie tax does not apply; one safe harbor is that the kid is at least 24 at the end of the year in which the stock is sold. Read the full article here.

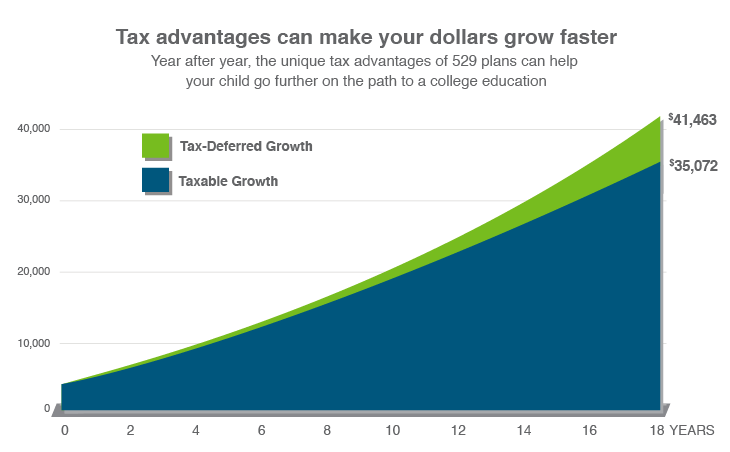

2 extracting tax savings from 529 savings accounts

Money compounds tax-free in these 529 savings accounts, provided that it’s used for things like tuition, room and board. Some agility is needed to keep the savings safe from financial aid formulas. The Forbes article mentions that another benefit is that many states subsidize these accounts by handing the donor an income tax credit or a deduction for contributions.There is also an estate-tax angle: A grandparent can pre-claim five years of gift tax exclusion to park $75,000 per youngster in college savings. That gets the money out of the grandparent’s estate, provided this person lives five years, while leaving the grandparent with some wiggle room to take the money back later.

Money compounds tax-free in these 529 savings accounts, provided that it’s used for things like tuition, room and board. Some agility is needed to keep the savings safe from financial aid formulas. The Forbes article mentions that another benefit is that many states subsidize these accounts by handing the donor an income tax credit or a deduction for contributions.There is also an estate-tax angle: A grandparent can pre-claim five years of gift tax exclusion to park $75,000 per youngster in college savings. That gets the money out of the grandparent’s estate, provided this person lives five years, while leaving the grandparent with some wiggle room to take the money back later.

Where it can get tricky relates to how the accounts interact with financial aid formulas. If, as in the typical arrangement, the account owner is the parent, the aid office treats it as other family assets, like a bank account balance; in that case, roughly 5% of the balance gets dinged every year via reduced aid. If a grandparent owns the account, it’s usually withdrawals, not balances, that are assessed and the damage is worse. Mr Baldwin suggests that defense strategy that can be used is for a grandparent to own the account and play musical chairs with beneficiaries. His example is “let’s say the intended beneficiary is Sally, soon headed to college. Grandpa names Sally’s 8-year-old cousin as beneficiary, meaning the money appears nowhere on any balance sheet of Sally or her parents. Just in time to pay for Sally’s senior year, Grandpa switches the beneficiary to Sally and disburses the money.” In this scenario the disbursement comes too late for the financial aid officer to take it into account as a reduction in need-based aid.

3 Optimizing the IRA to Roth conversion

You can prepay income tax on some of your IRA, making future withdrawals tax-free. This is very clever if (a) your tax bracket is fairly low at the moment, and (b) you can cover the tax bill with money from outside the account. Beware that conversions cannot be undone, it’s a good idea to do some calculations before taking the plunge. Use your tax software to see what the extra income will do. Here’s just one peculiarity: The 3.8% Obamacare surtax ostensibly does not apply to conversion amounts, but in fact it does for certain unfortunate taxpayers.

The 3.8% hit applies to the lesser of investment income or the amount your joint-return income tops $250,000. Suppose you have $200,000 of salary income and $60,000 from capital gains and dividends. Only the last $10,000 of that investment income is now exposed to the surtax. But what happens if you toss a $40,000 conversion into the mix? The conversion amount counts as income, so your adjusted gross climbs to $300,000. That boosts an incremental $40,000 of investment income into surtax territory. When it’s all settled you have, in effect, paid a 3.8% tax on your conversion.

Roth IRA accounts (are a special retirement account where you pay taxes on money going into your account, and then all future withdrawals are tax-free) have benefits not only for the account owners but potentially for their heirs as well. The heirs get the money without owing income tax on it. The prepayment of income tax, moreover, is itself a nice gift from the original owner, and this tax asset appears nowhere on any gift or estate tax return

The Secure Act of 2019 tightened rules on inherited IRAs, including Roth IRAs, but even now the heirs can take their time (ten years) liquidating an account. Mr Baldwin has written about the value of ‘Rothifying’ (a term he coined it seems) with a calculator that you can download from Roth Strategy After the Secure Act: Calculate Your Benefit. His perspective is that Rothifying pays off surprisingly often.

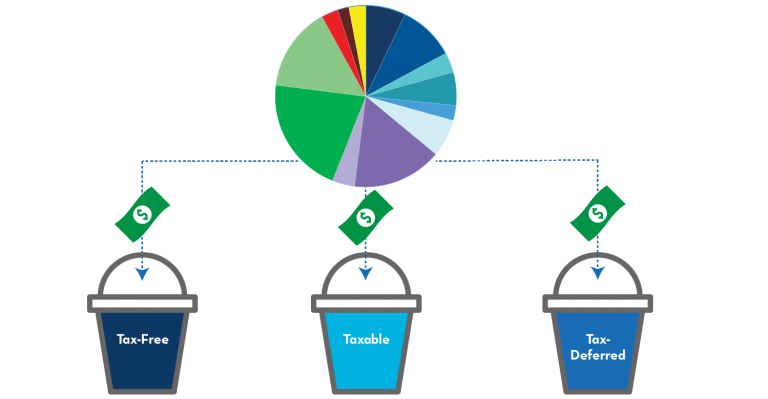

4 Investment portfolio allocation

(image credit: Pure Financial)

Mr Baldwin explained that there are good places and bad places to park certain kinds of investments. Swapping locations can save a bundle at tax time. Move junk bonds and commodity funds out of your taxable account into your IRA. Go the other way with your stocks, especially foreign stocks. So retirement portfolios can have a few different slots that you can allocate money:

- a taxable brokerage account,

- pretax 401(k)

- or IRA retirement accounts and a tax-free Roth account

The Forbes article author suggests that the taxable account is a good place to put most common stocks and the funds that own common stocks. There they get the benefit of a favorable tax rate (15% for most investors) on dividends and long-term capital gains. You can read the full article here, where the author discusses a few different types of assets such as bonds, REITs, and deciding between taxable accounts and tax-favored retirement accounts. He says that once you have figured out which assets that belong in retirement, you then must decide between things to put in the pretax IRA and which in the aftertax Roth acct. Mr Baldwin suggests ”select the riskier, higher-return items for the Roth account. “ Because the The Roth has no mandatory withdrawal during your (or your spouse’s) lifetime, so you can let it sit and grow.

5 take advantage of tax benefits from side hustle business

(image credit: healthsherpa)

So if you are not a small business owner or partner in a company and you work a professional as a salaried employee, there are some tax benefits that you might be missing out on. So Mr Baldwin suggests that if you and your spouse started a business, in his example you could raise purebred show dogs, stating “ you can deduct things like dog show expenses that would never be deductible from salary income.” From what’s left after business expenses you can deduct half of what this sideline costs you in Social Security and Medicare taxes.

Next, if your employer from your day job does not provide an employer-subsidized health plan, you can possibly get the self-employed health insurance deduction. According to a TurboTax article, you can only claim the health insurance premiums write-off for months when neither you nor your spouse were eligible to participate in an employer-subsidized health plan. This health insurance write-off claim is entered on page 1 of Form 1040, which means you benefit whether or not you itemize your deductions or use the standard deduction. Unlike an itemized deduction, this deduction treatment is beneficial because it lowers your adjusted gross income (AGI). Having lower AGI can reduce the odds that you’ll be affected by unfavorable phase-out rules that can cut back or eliminate various tax breaks.

AGI is used in all sorts of formulas to punish higher-income taxpayers.

The forbes article author explains with this example, that there is more from this fictional dog show company. Let’s say you have $60,000 left after the dog shows, the half of the payroll taxes and the health insurance premiums. If you take the Section 199a 20% Qualified Deduction for Pass-through Income gives you a $12,000 deduction on your federal taxable income. That means you owe federal income tax on only $48,000. This pass-through deduction for business owners that do not pay the corporate income tax rate that was created under the 2017 Tax Cuts and Jobs Act (TCJA), is set to expire at the end of 2025. Congress may move to crack down on corporate tax cuts for large companies. But it is probably less likely that legislators will go after laws that hurt self employed electricians and dog breeders (LOL).

Even if you don’t take the pass-thru deduction, Mr Baldwin points out in his scenario example, that you could use the $60,000 to calculate permissible contributions to retirement. One option is to set up a self employed “solo 401k” plan. So certain requirements need to met, but if neither you or your spouse are making 401(k) retirement contributions in your corporate employed day job, and if you both are over the age of 50, then you can send #52,000 off to a tax-free Roth account.

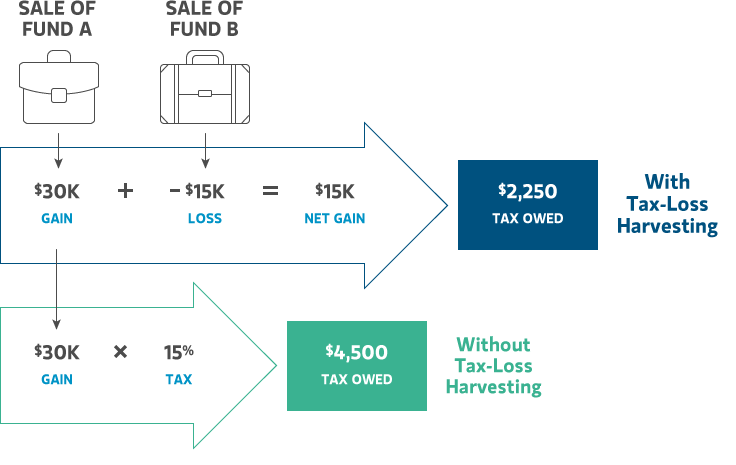

6 Take advantage of tax harvest losses from a well balanced investment portfolio

(image credit: morgan stanley)

One of the oldest rules of our tax code, is that gains and losses are recognized only on the sale of property. Of course there are some exceptions to this rule, such as something called commodity futures, but they or not so common. There is a technique used in investment taxable brokerage accounts; called tax loss harvesting, which is the strategy of the selling of securities at a loss to offset (booking capital losses) a capital gains tax liability. An Investopedia article states that “this strategy is typically employed to limit the recognition of short-term capital gains. Short-term capital gains are generally taxed at a higher federal income tax rate than long-term capital gains. However, the method may also offset long-term capital gains.” As the Forbes author mentions that mart investors are happy to sell losers while hanging onto winners. He says “if you have 40 stocks, 35 of them up from their purchase price and five down, you’d sell the five stinkers and replace them with similar but not identical investments (for example, you replace an oil stock with an index fund of oil stocks).” This recent Reddit Gamestop trading frenzy is bringing stock trading and short term capital gains taxes into the news cycle. Nerdwallet has a pretty thorough article on capital gains taxes.

- Capital gains taxes can apply on investments, such as stocks or bonds, real estate (though usually not your home), cars, boats and other tangible items.

- The money you make on the sale of any of these items is your capital gain. Money you lose is a capital loss. Our capital gains tax calculator can help you estimate your gains.

- You can use investment capital losses to offset gains. For example, if you sold a stock for a $10,000 profit this year and sold another at a $4,000 loss, you’ll be taxed on capital gains of $6,000.

- The difference between your capital gains and your capital losses is called your “net capital gain.” If your losses exceed your gains, you can deduct the difference on your tax return, up to $3,000 per year ($1,500 for those married filing separately).

- Capital gains taxes are progressive, similar to income taxes.

That harvesting or “tax-loss selling” gives an investor capital losses that can be used to absorb any amount of capital gains plus up to $3,000 a year of ordinary income. Now if you follow the strategy of being a long term investor by hanging on to winner stocks you can avoid most capital gains, but you will not completely avoid gains. Because they can happen as a result of cash mergers or distributions on mutual funds, so a coffer of capital losses to draw on can be very useful. Bonus any unused losses can be carried forward indefinitely.

Mr Baldwin points out that some portfolio money managers do this type of strategy on a larger scale, by using algorithms for automated loss harvesting from huge portfolios that look like index funds. He mentions a firm called Parametric Portfolio Associates, where the CEO Brian Longstraat, explains that “that automated harvesting can deliver a percentage point a year, or more, of incremental after tax return during the first decade after a portfolio is created.” Eventually, the customer winds up with all positions in the gain column, so no further tax benefit can be extracted. But during that first decade the tax benefit is likely to amply cover the manager’s fee.

If you aren’t selling winner stocks, what do you do with them?

Mr Baldwin gives 3 tips.

- You can give appreciated assets away to low-bracket by shuffling assets to sidestep capital gain taxes.

- You can leave them in your estate to benefit from the step-up.

- And you can donate them to a donor-advised fund for charities.

The final caveat about this tax saving technique is that: Congressional tax reformers are on the prowl, and there are various ways they could make this time-tested strategy less appealing. Such as taxing investors on paper gains, the way commodity futures are now taxed. Although it might be difficult for them to implement. Another threatened tax change is to end the step-up in the basis of assets at death. That change might hit everyone, or, more plausibly, only families with assets worth millions. A change to this tax law might treat death as a sale, creating an immediate tax obligation, or it might merely have the heir pick up the old cost basis. If Congress were to change this tax law it might have some adverse ramifications such as that it would result in the forced sale of many occupied homes or property. .

7 Take advantage of a health savings account (HSA)

The Forbes author describes a personal income taxes savings strategy of utilizing a health savings account, as a perfect trifecta:

- It delivers a deduction

- tax-free growth

- and a tax-free withdrawal

If you have a high-deductible health insurance plan, you (or your employer) can put money into an HSA, getting a deduction on the way in. As it was mentioned earlier in number 5, that this tax deduction treatment is one that reduces adjusted gross income (and thus is more valuable than most itemized deductions). The money compounds tax-free, just as it would in an IRA. What is great is that years down the road, you can take it out tax-free if you use it to cover out-of-pocket medical costs incurred after you joined the high-deductible plan. Mr Baldwin states that “if you play your cards right, the HSA beats a plain old IRA, which is going to be taxed on exit if it’s deductible on the way in.” Similar to IRAs, HSAs can be invested in stock index funds and other things with generous long-term rewards. Health Savings Accounts (HSAs) were created and designed to help people offset health care costs in a tax efficient way.

So how can you take advantage of this strategy? Try to avoid the usual pattern of using HSA balances to immediately cover your co-pays and deductibles. Instead, pay those things out of your checking account. But hold onto your medical bill receipts. Now if you let the HSA compound, tax-free, for a decade or two. At some point well into retirement, fish the receipts out of a drawer and you can use them against a tax-free withdrawal from the HSA.

If you use an HSA in this way, then you have a super-IRA to pay for retirement living. “if the HSA balance exceeds cumulative medical expenses (unlikely), the excess becomes a standard IRA, taxable on exit.” said Mr Baldwin.

8 Exercise an Incentive Stock Option in January hold them 11 months

What are Incentive Stock Options (ISOs), Investopedia defines them as “a corporate benefit that gives an employee the right to buy shares of company stock at a discounted price with the added benefit of possible tax breaks on the profit.” ISOs also are called statutory or qualified stock options. Basically it’s an IRS term for a special kind of employee compensation benefit that has a potential tax-favored payoff. The deal involves getting long-term capital gain treatment on what is, in effect, compensation for labor. The profit on qualified incentive stock options is usually taxed at the capital gains rate, not the higher rate for ordinary income. Non-qualified stock options (NSOs) are taxed as ordinary income. Some of the key takeaways include:

- Incentive stock options (ISOs) are popular measures of employee compensation received as rights to company stock at a discounted price at a future date.

- These are a particular type of employee stock purchase plan intended to retain key employees or managers.

- Usually, incentive stock options require a vesting period of at least two years and a holding period of more than one year before they can be sold.

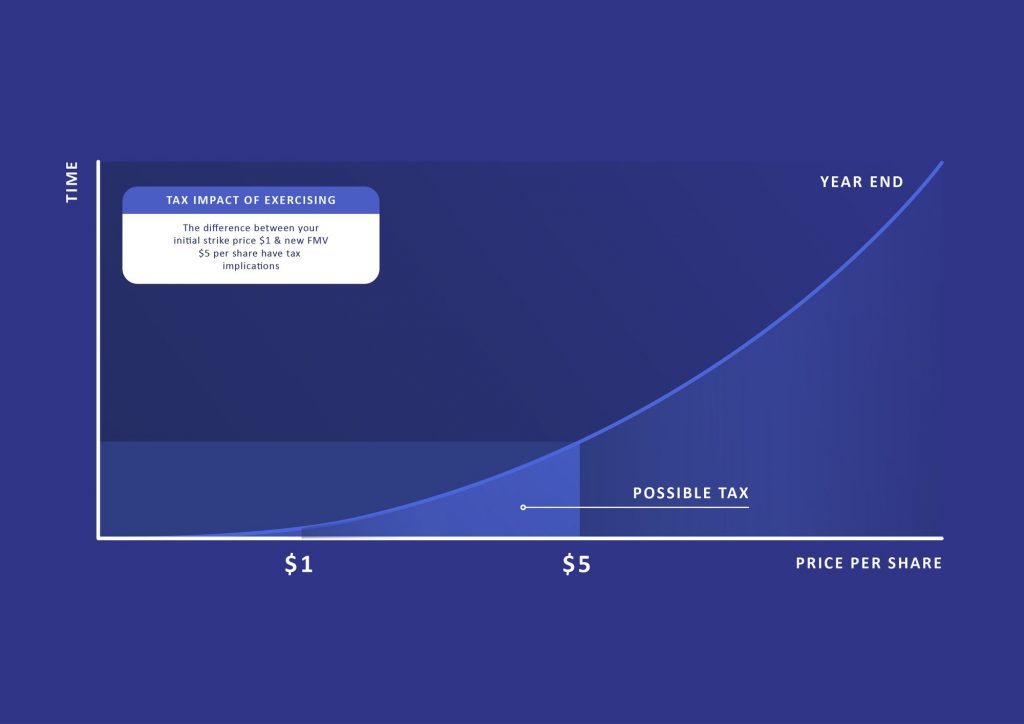

ISO’s have rules and vesting schedule limits. An article in yearend.com says “the ISO is issued on a specific date (called a grant date) and the employee can choose to purchase the stock (exercise the option) at a predetermined price known as the strike price. Mr Baldwin gives a scenario example to explain more. In any calendar year you can get these options on only $100,000 worth of stock. Let’s say you get an option on 20,000 shares, with a strike price of $5, when the shares are worth $5. And let’s say the company ends up being successful. When the stock is worth, say, $20 a share, you exercise the option. You write out a check for $100,000 and acquire shares worth $400,000. You have made an instant paper profit of $300,000.

The goal is to have that $300,000 taxed as a long-term gain, which is a gain on an investment held for longer than a year. This is doable, but the downside is that the $300,000 is potentially subject to “alternative minimum tax.” AMT is calculated based on your regular income minus some personal deductions (such as local or state sales tax). If you have an ISO, you’ll also need to factor in the spread between the price of exercising your ISO and its fair market value (FMV) at the time of exercising. The alternative tax regime runs in parallel with the regular tax, and you owe the higher of the two.

One way to avoid getting hit with the AMT tax, If you sell the shares in the same year as exercising the option, the difference between the sale price and $5 is treated as ordinary income and the AMT problem vanishes. In other words, if you are willing to give up any hope of getting long-term treatment of your gain, you can ignore the AMT threat altogether.

If, on the other hand, you can hold your breath for a whole year after using the option to buy shares, and you also hold the stock until at least two years after the option was handed to you, the difference between the sale price and $5 is a favorably taxed long-term capital gain. That favorable rate on regular tax can make up for the potential liability from the alternative tax. You can read more from Mr Baldwin’s article on ISO strategies, but he explains “exercise an option in early January after holding that option for at least a year. Then look at the stock in late December. If it’s down from where it was at exercise (say, it drops to $12 in our example), you sell and pay ordinary income tax on whatever profit is left ($7). That protects you from having $15 of phantom AMT income when you’re only $7 ahead.”

Scenario 2

If the stock is up in late December (let’s say, to $45), you hold on for a little longer. If you sell in mid-January, that will be more than two years after you got the option and more than a year after you turned the option into stock. Then the whole gain ($40) is taxed at a favorable rate. There would still be some AMT income ($15 a share) for the previous year, but this will be tolerable if you’re making a killing on the stock and if that profit is favorably taxed for non-AMT purposes.

9 Use QSBS to get $10 million tax-free from a startup

You can get a tax-free bang from a small number of bucks by investing in a corporation when it’s small. Section 1202 is how some people get rich in Silicon Valley. To help entrepreneurs spur innovation, Congress has granted a tax exemption on capital gains from small companies. Small here is defined as having no more than $50 million in assets when an investor buys in. The deal is codified in the tax code’s Section 1202. In 2019 I wrote about this tax law loophole which is called the Qualified Small Business Stock, or QSBS, exclusion. To qualify for this exemption you must get your shares from the company, by purchase or labor, rather than in the secondary market; you must hold on for five years, and you must have bought after 2010. The tax free capital gain is good for an exemption on the greater of $10 million or ten times your purchase price.

Three cheers for small, struggling enterprises. If there were 500 investors each chipping in $100,000 to start the next Apple, they could collectively exclude $5 billion of capital gain when they cash out.

Fodder for reform? Maybe. But note that startup lottery winners tend to work in technology, a sector that donates to progressive causes. Section 1202 will probably be around for a while.

Conclusion

While tax rules and rates may change over time, the value of keeping taxes in mind when making investment decisions does not. The reason? Taxes can reduce your investment returns from year-to-year, potentially jeopardizing your long-term goals. We will pay attention to any potential tax changes that the Democratic administration may propose over the coming years.

The higher your current income tax rate, the more beneficial it may be for you to consider the impact of taxes when making changes to your investments. Be sure to consult with your professional tax advisor before making any decisions that could affect your taxes. Feel free to contact Huckabee CPA if you have any questions for a free consultation.

{kind=link}